Italy’s eyewear industry fears a minus of 25 percent

von Redaktion,

ANFAO, the Italian Association of Optical Products Manufacturers, has published the economic figures for 2019 and the first months of 2020, but after a very respectable last year, the forecasts for Italy do not bode well for the eyewear industry this year due to the economic consequences of the corona crisis.

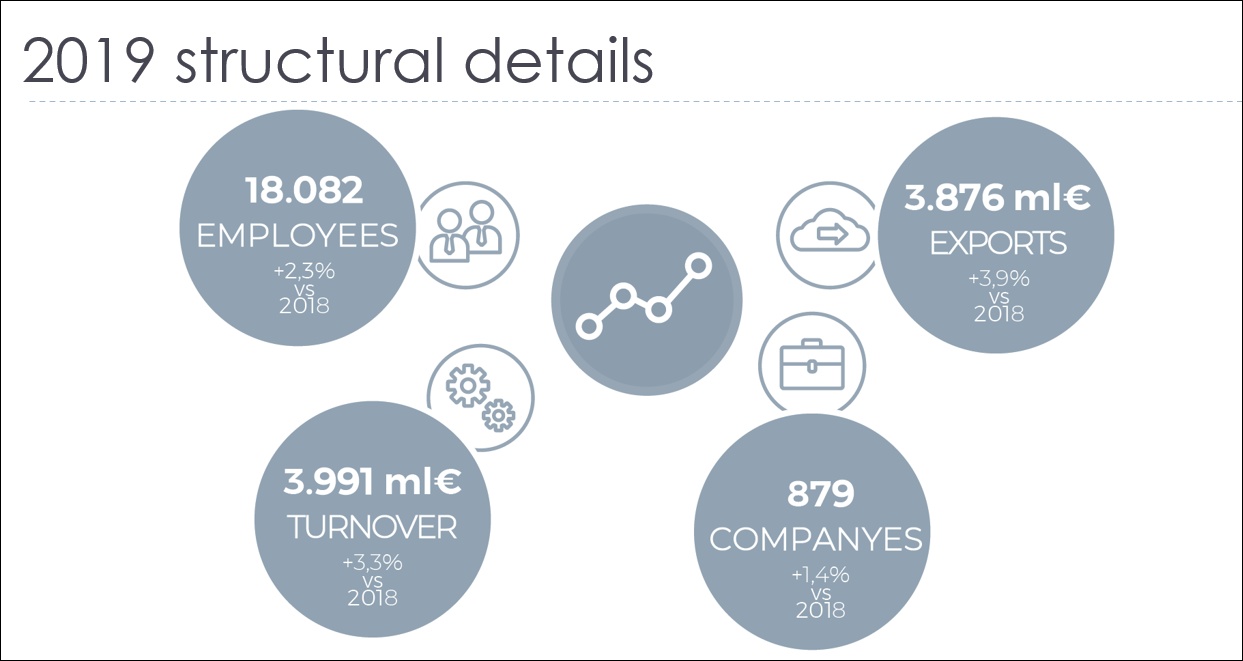

Italys Eyewear Market 2019

The global economy experienced an overall slowdown in 2019. In Italy, 2019 unfolded against the backdrop of an ailing domestic market and a sluggish economy. Despite these difficulties, 2019 was a fairly decent year for Italian eyewear, with reassuring results.

Anzeige

Indeed, Italian eyewear production in 2019 totaled 3,991 million euro, 3.3% higher than in 2018, so ANFAO. The number of companies stayed fairly constant with 879 businesses nationwide, up 1.4% compared to the previous year.

Eyewear Market in 2019 (Source: ANFAO)

In terms of jobs, the year ended on a good note, although the first signs of trouble from some of the large groups appeared ominous: at year-end 2019, jobs numbered 18,082, a 2.3% increase over 2018.

2019 Exports and Imports

Representing 90% of the sector’s overall production, exports of frames, sunglasses and lenses grew by 3.9% over 2018, for a total value of 3,876 million euro. In 2019, exports of sunglasses increased 2.8%, valued at about 2,584 million euro. On the other hand, frame exports grew 6%, totaling approx. 1,201 million euro.

Imports experienced a similar upward growth trend of 6.7% equal to about 1,347 million euro, substantiating the industry’s vitality. The Italian eyewear industry’s trade balance continues to be largely in surplus (putting the 2019 export-import balance at 2,530 million euro).

Exports by Countries

Looking specifically at the two product macro-segments – sunglasses and frames – by geographic area, we can see that: The primary market for eyewear exports in 2019 continued to be Europe (claiming just under 50% of all eyewear sector exports) for an upward growth trend of 2.2% (+3.2% sunglasses, +0.4% frames).

In America (area to which about 33% of Italian eyewear exports are shipped), 2019 saw a 6.7% increase in sun-optical sector exports, compared to 2018. Driving this growth spurt was the outstanding +12.3% performance of frame exports along with a healthy +4.6% jump for sunglasses.

In Asia, the continent that claims more than 16% of Italian frame and sunglasses exports, 2019 export growth trended upward by 3.4%, and turned 2018 performance on its head with a drop in exports of sunglasses (-0.7%) and a major increase in frames (17.4%).

Africa is an area that claims less than 2% of current sector exports; although still untapped, it shows good potential for growth. In 2019, frame exports grew in value by 12.8%, while sunglasses remained basically unchanged (+0.1%).

In Oceania, a still marginal area with a less than 0.5% share, Italian exports of sunglasses and frames in 2019 decreased 14.5% in value compared to 2018.

As regards imports, Asia was, once again, the primary supply market in 2019 with a nearly 75% share, concentrated almost exclusively in East Asia.

The export analysis by individual country

In the United States, (which has long been the eyewear industry’s primary export market, with an almost 27% share), overall exports of frames and sunglasses increased 6.7% over 2018. Growth occurred in both sectors: the value of frame exports increased 12.8%, and exports of sunglasses 4.6%.

In Europe, the performance of Italian exports to the various countries was impacted by the general economic situation, Brexit concerns, the reorganization of healthcare reimbursements in France and the general slowing of domestic consumption. Against this backdrop, our exports encountered even stronger headwinds in France and the UK.

In France exports for the sun-optical sector in 2019 decreased 3% in value (-4.4% for frames and -2% for sunglasses). The outcome achieved by Italian eyewear exports to the United Kingdom once again reflected Brexit-related concerns: thus, exports lost 7.9% in value overall, compared to 2018 (-9.8% for sunglasses, -3.1% for frames).

Eyewear exports performed a bit better in Spain, where the growth trend fell just 0.3% compared to 2018, with exports of sunglasses making positive gains (+1.6%) that offset the negative frame results (-4.7%).

Instead, in Germany, Italian eyewear exports fared very well: with an overall growth rate of 8%, up 10.1% in sunglasses exports and +4.9% in frames.

Rounding out the list, eyewear exports to the BRIC countries which, taken together, claimed about 8% of the industry’s exports. For a bloc of countries this size, it is still a fairly meager share; nonetheless, it is a bloc with enormous potential (China alone claims 5% of eyewear exports): Brazil +6.9% (+2.1% sunglasses +14.3% frames), Russia +19.4% (+23.3% sunglasses and +13.7% frames), India +7.1% (+6.4% sunglasses and +8.9% frames) and China +2.4% (-1.2% sunglasses and +13.9% frames).

The Italina Global Export Market Share

Based on the global export market for sunglasses and frames, in 2019 worth just under 19 billion euro (+5%), the Italian market share is valued at more than 20%, second only to China. If only high-end exports were taken into account, Italy would still be in first place with a nearly 70% share in value.

Exports by Volume

The Italian eyewear industry exported about 103 million pair of eyeglasses in 2019, slightly more than in 2018 (+1.9%). Of the total number of pairs exported, 66 million were sunglasses (64%) and 37 million optical frames (36%). Specifically, sunglasses exports (+0.6%) were fairly stable, while optical frame exports grew by 4.3% compared to 2018.

The Domestic Market

Between exports and the domestic market, it could be said that the Italian eyewear industry ended 2019 on split levels: excellent performance in international markets collides with the weakness of the domestic market.

Consumption, monitored by GfK on the specialized eyewear channel, decreased slightly and remained stagnant compared to the two previous years: -0.2% for an overall value of approximately 2.9 billion euro.

There was no relief from the negative trend in sunglasses (-2.4%) and frames (-2.6%), unlike the performance of ophthalmic lenses (+2.5%) which, in terms of revenue now account for more than 46% for point of sale outlets (thanks to high-added-value segments like progressive lenses that manage to sustain a positive trend).

As in 2018, also in 2019, the upward market trend for frames and sunglasses remained focused on high-end (luxury), and low-end (i.e. private label) products, to the detriment of mid-high range offerings. Also, with regard to sunglasses, the market share of traditional optical channels continued to decrease, shifting in favor of online sales channels.

2020: Covid-19 Crisis in Italy

The year 2020 opened to signs of global uncertainty. Events in the Middle-East, first and foremost the US-Iran conflict, heralded more unpredictable prospects than ever. For Italian eyewear, there were signs of a slowdown in global exports and a jobs situation that hinted at a possible labor downsizing tied to the performance of several specific companies.

Then the threat of a virus similar to SARS appeared that led to woeful forecasts of financial troubles in relationships with Asia, but certainly nothing compared to what the global pandemic ushered in. In January, the Ccovid-19 crisis spread from China to all of Asia. This initial phase immediately caused difficulties for those industry businesses that export 90% of their products.

Exports to China, Hong Kong, Macao and Taiwan (the first Asian countries subjected to restraints) account for 7.7% of all industry exports (just under 300 million euro/year). China, Hong Kong and Taiwan are also the leading suppliers of raw and semi-finished materials for Italian eyewear. As to imports, the above-mentioned countries account for 64% of all sector imports (about 700 million euro/year).

In addition to the impossibility of exporting to Asia, companies had to deal with the lack of raw and semi-finished materials. To address this situation, they turned to different supply markets, incurring higher costs in the process. In addition, some large companies with production plants in China (primarily serving China and neighboring markets), had to halt production.

ANFAO: “On February 22, the day the first patient was identified in Codogno (Northern Italy), the unthinkable became reality. Italy entered one of the darkest and most tragic moments since the post-war era and a global pandemic was declared. The eyewear sector lost its leading international trade show, MIDO, which was postponed to 2021, and the country underwent 60 days of lockdown.”

The eyewear companies that produce medical devices (optical eyeglasses) and personal protection (sunglasses) were considered essential, basic necessities. For the same reason, opticians were authorized to keep their businesses open.

“Despite this option, once the companies complied with the obligatory safety requirements, many had to resort to unemployment compensation programs because international orders suddenly dropped to zero. On the domestic front, the opticians who decided to stay open, did so almost exclusively to cater to the needs of urgent cases of broken eyewear and little more,” stated Giovanni Vitaloni, President of ANFAO and MIDO.

The first Quarter of 2020

In terms of exports, Italian eyewear closed Q1 2020 with a 17.7% loss, about 200 million euro less than in Q1 2019. This loss was concentrated primarily in the month of March (-43.6%), while January closed out in line with 2019 (+2.9) and February only felt the effects of the difficulties in Asia (-3.8).

From a geographic standpoint, the eyewear industry suffered significant Q1 losses in exports to America (-20.3%), Europe (-16.5%) and Asia (-16.3%).

In terms of the domestic market, the months of January and February were in line with 2019, but March (bearing in mind the lockdown which began in the second week), brought losses of 30% in volume and revenue. April was emblematic with 80% losses; May brought the beginning of a turnaround, but nonetheless closed at -33% in terms of sell-out.

2020 Forecast

The first part of 2020 was certainly challenging for the eyewear industry, in several ways. President Vitaloni’s analysis: “Undoubtedly, the cancellation of the trade shows did enormous damage to our companies, consistently focused on exports, who view the fairs themselves as a means of internationalization. Furthermore, cancelled meetings and contracts, aborted travel plans, the impossibility to fulfill orders and the cancellation of previous purchase agreements were the order of the day in the first part of 2020.

Regardless of these direct effects, we cannot overlook the increased costs tied to managing fallout from the pandemic: the inability of agents to call on clients, adaptation to remote working for office staff, implementation of safety procedures and protective measures for employees, adaptation of the workplace, along with implementation of new ways to present products – ranging from digital showcases to the production of new samples to be shipped at increased logistic costs.”

ANFAO forecasts for exports, based on currently available data, estimate negative monthly results (with peaks from April to July 2020) up to year-end. Also considering that export levels in 2019 were moderate and unlikely to be repeated under the current conditions.

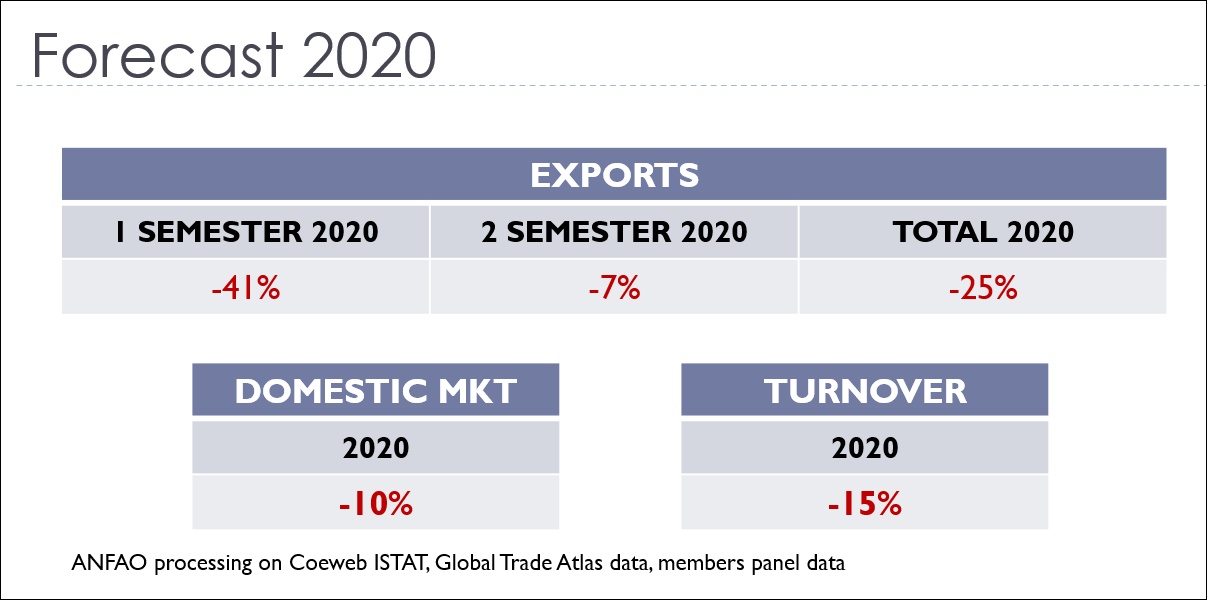

The first half of 2020 could close with 40% fewer exports (in terms of value, more than 850 million less than in 2019). Based on a recovery in the second half of the year, compared to the first half, without factoring in possible new outbreaks of the crisis, the second half of 2020 could suffer a -7% in value (about 130 million less).

Forecast 2020 for Italy’s Eyewear Industry (Source: ANFAO)

Overall, the forecast for Italian eyewear exports in 2020 could suffer a 25% loss, equal to nearly 1 billion euro.

As regards the domestic market, considering the previous and current difficulties that have significantly aggravated the situation, the forecast for year-end is for at least a 10% loss in value. Likewise, production could decrease by about 15 percentage points.

“We were very cautious in making these forecasts – confirms the ANFAO President – After all, the feeling we get from our member companies doesn’t allow for any more optimism than that. We know the situation is dire for the entire country and that is why we joined the move to ask for truly effective measures to support the economy and consumption.

Among these, I am pleased to mention our own request, made under the aegis of the Eyecare Commission, for a voucher to purchase prescription eyewear, to at least lend a minimal boost to consumption and, at the same time, focus attention on the importance of vision, that could take a back seat in times like these.

Another key aspect is for the export machine to get back into operation again as quickly as possible, and that the highly publicized export agreement becomes a concrete reality. Thanks to the reopening of the trade shows that are vital to our companies. I am still optimistic about that and we continue to work with all our might to make sure that DaTE first and, above all, MIDO, can mark the true relaunch of our sector.”

Summary Data Graphs and Charts: Computations by ANFAO and Confindustria Moda for ANFAO based on data from ISTAT, Coeweb, Global Trade Atlas, INPS and CCIAA